An important question frequently asked is ‘What is the cost of an audit?’ and ‘What time does it take to do an audit?’.

It is fair to say that competition within the profession is fierce right now, and firms are struggling to balance compliance with regulation and surviving in a competitive environment. Audit firms are ‘under-cutting’ each in attempts to secure the assignment. Audit firms are like their clients – they work to make a profit

Moreover, practitioners are subject to rigorous legislation and standards from regulatory bodies such as HMRC and Companies House. All statutory audits must be done in accordance with the Individual Savings Accounts (ISAs).

Duties of an auditor

Auditors must produce work in accordance with prescribed standards which are required by professional institutes, in addition to their duty of care to the client, like the follows:

- Ensures compliance with established internal control procedures by examining records, reports, operating practises, and documentation.

- Verifies assets and liabilities by comparing items to documentation.

- Completes audit workpapers by documenting audit tests and findings.

- Appraises adequacy of internal control systems by completing audit questionnaires.

- Maintains internal control systems by updating audit programmes and questionnaires; recommending new policies and procedures.

- Communicates audit findings by preparing a final report; discussing findings with auditees.

- Complies with federal, state, and local security legal requirements by studying existing and new security legislation; enforcing adherence to requirements; advising management on needed actions.

- Prepares special audit and control reports by collecting, analysing, and summarising operating information and trends.

- Maintains professional and technical knowledge by attending educational workshops; reviewing professional publications; establishing personal networks; participating in professional societies.

- Contributes to team effort by accomplishing related results as needed.

The increasing number of audit firms and technology in the audit process have brought the average cost of audit services down.

The answer to both questions, still is ‘it depends’.

It depends on other factors like complexity of the assignment, the available resources, the timescale involved and the degree of risk.

The UK audit sector

All companies in the UK are required, under the Companies Act, to have their annual accounts audited externally, unless exempt. A company’s auditor must make a report to the company’s members on the accounts produced, and for public companies these reports are laid before the company in a general meeting. For Public Interest Entities (PIEs), audit committees typically have a key role in the selection, appointment and removal of auditors, as well as agreeing the terms and fees to be paid, and making recommendations to the company board concerning these matters.

There are many audit firms in the UK that can carry out these statutory audits, but few such auditors currently audit the largest publicly listed companies, including those listed on the FTSE 350. The FTSE 100 and 250 collectively are referred to as the FTSE 350.

The large auditors in the UK are part of similarly branded international networks of audit firms. Audit firms in these networks are experienced at working together to provide international companies with a seamless audit service across borders, so a company may only need to appoint one single auditor for its global business.

Big Four and the Challengers

In the UK, 97% of audits of FTSE 350 companies are undertaken by the Big Four auditors, which are PricewaterhouseCoopers (PwC), KPMG, Ernst & Young (EY) and Deloitte. While there are many smaller audit firms that carry out audits for unlisted and smaller companies, there are several challenger firms, some of which have a small number of clients in the FTSE 350. Challenger firms include BDO, Crowe, Grant Thornton, Mazars and RSM. Many challenger firms have international networks of firms like the Big Four, although these are more limited.

There has been consolidation in the audit sector in the last 30 years. Before 1987, there were eight large international audit firms in the UK, and there have been four large audit firms since 2002, following Arthur Andersen’s demise that year and the merger of Price Waterhouse and Coopers & Lybrand in 1998.

Cost of an audit

As mentioned earlier, it is difficult to measure a common cost charged for audit by firms.

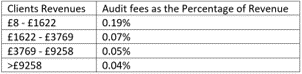

However for the purpose of calculating an average cost of an audit as a percentage of the revenues of the clients, one of the researches by Audit Analytics has come up with the following table:

Between 2010 to 2016, audit fees increased steadily, climbing to £7.16 billion in 2016 from £5.92 billion in 2010.

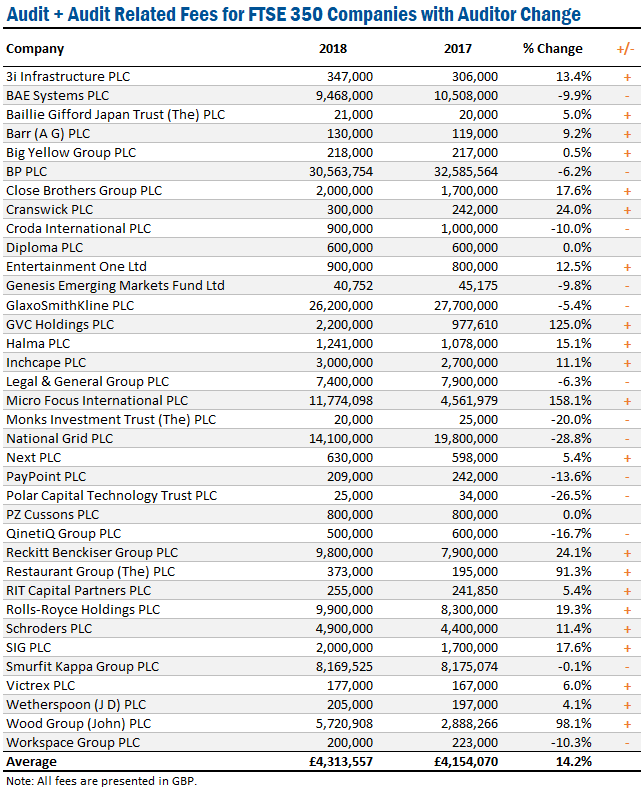

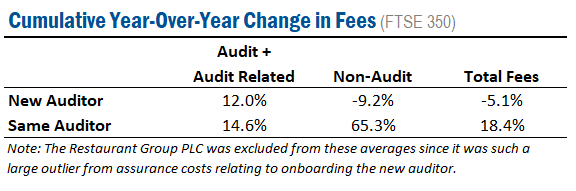

According to Audit Analytics, for the FTSE 350 Auditor Changes and Fees, the following were the audit and audit related fees for FTSE 350 companies with auditor changes:

Comparing this data to 2016-17, in the year 2019-18, more than 3/4th of the companies in the list saw their fees increase by an average of 21.7%, while a handful of 1/3rd companies saw their fees decrease by an average of 7.2%.

Time to do an audit

For a typical £7 million turnover company with good internal controls, sound structure and no prior year problems or current ‘extraordinary’ problems, planning alone should take a good couple of days (certainly at least one day and that is being overly generous), if the work is done in accordance with the ISAs, as this would involve the audit team planning meeting, discussions with the client, updating the permanent file, reviewing the engagement letters (and updating if necessary), building the planning notes, performing initial analytical procedures and developing the audit plan. Then comes the detailed fieldwork.

If firms are involved in the accounts preparation side of things then audit evidence can be obtained from the accounts preparation file which could reduce the time spent on the detailed testing, but if not then audit firms will have to consider how they are going to gather the evidence to support the amounts and disclosures in the financial statements; this evidence is not just agreeing the amounts in the financial statements to the trial balance. For a first time audit this process will often take longer due to having to get a thorough understanding of the client and performing audit work on the opening balances.

Completing an annual audit

- For completing an annual audit, the following steps need to be followed:

- Discussing with the auditor the need for assistance and establish a high priority for agreed-upon items, while ensuring the time frame is fair to the staff.

- Expressed needs, as well as the audit procedures that will be performed must be discussed with management.

- Determining contact people for specific areas under audit and avoiding any potential scheduling conflicts, such as vacations, scheduled medical procedures, work schedules, out-of-town needs and holidays.

- Establishing an ‘auditor’ file for regulatory agency correspondence and for copies of new or changed documents about fixed asset additions and disposals, debt agreements, leasing arrangements, lawsuits, complex transactions, technology modifications and major customers and vendors.

- Reconciling detail to general ledger account totals. For example, reconcile all bank accounts, accounts receivable, accounts payable and equipment lists. Requests should be made for templates, copies of prior working papers and clarification so that you can prepare information in a format acceptable to the auditor.

- Preparing deadlines to discuss significant estimates used in the financial statements, such as allowance for uncollectible accounts, warranty reserves and percentage of completion.

Conclusion: No menu for cost and time

If firms are undercutting other firms of auditors (sometimes referred to as ‘lowballing’) then sacrifices must be made and in some unfortunate cases, these sacrifices are in the quality of the audit work. Firms who deliberately undercut in attempts to get the client’s audit onto their books must still be prepared to do the work in compliance with the standards.

Firms who are subject to fee pressures from their client, or who deliberately undercut another firm to secure the audit run the risk of cutting too many corners in order to make the audit worthwhile in terms of cost.

Professional regulators have always had a ‘gripe’ about audit firms who do not devote enough time to audit planning, or who express an unqualified audit opinion when they (knowingly or not) have failed to generate enough evidence to support that opinion.

There is no set timescale as to how long an audit should take, nor is there a ‘menu’ of ideal cost to charge – it takes as long as it takes if it is to be done in accordance with the rules.