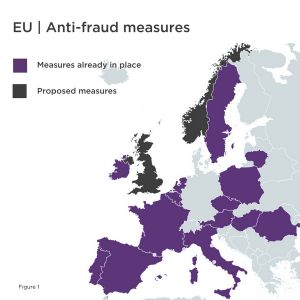

To date, 13 countries have implemented increased VAT reporting measures (and a further three countries have proposed measures), designed to tackle VAT fraud and close the “VAT Gap”. The VAT Gap is the overall difference between the expected VAT revenue and the amount actually collected, which the latest figures show stood at €159,460m in 2014 in the EU.

All the measures that have been introduced or are being proposed share similarities – the common traits being that they allow for an increase in controls and measures for the reporting of tax data. This allows tax authorities to much better audit a taxpayer’s records, in some instances in almost real time, enabling them to determine if the right amount of tax has been declared.

The consequence of this increased checking of data by the tax authority is questions being asked of taxpayers and audits being suffered by taxpayers. There has been a steady rise in the tax authority’s questioning of the tax treatment applied by taxpayers, with questions ranging from just asking for copies of invoices through to complete investigations of the VAT rate/liability applied. In all cases, it causes additional work and costs for a taxpayer alongside stress of not knowing what the outcome might be.

How have Member States adopted increased reporting in practice?

This map shows how many EU Member States have introduced increased reporting measures, or are proposing to do so in the upcoming years. These measures are outline below.

SAF-T

Many of the Member States that have introduced new reporting requirements have implemented SAF-T. This is a universally recognised accounting system which requires businesses to transmit data to the tax authorities in a unified electronic format.

Poland implemented SAF-T in 2016 and by introducing mandatory electronic filing the tax authorities have been able to introduce a level of automation to check on taxpayer returns. This has led to an increase in the efficiency of data checks, hence tax collection levels have increased and tax fraud has become easier to detect.

The Polish Minister of Finance estimates that the introduction of SAF-T should result in additional tax revenue of more than 17bn zlotys (approximately £3.5bn) within three years.

Romania has also introduced similar measures for businesses involved in Distance Selling and the Czech Republic now requires Czech VAT payers to file a control report alongside their periodic VAT returns. Both measures are intended to reduce the tax gap by discouraging fraud and making it easier for tax authorities to audit businesses.

Immediate Supply of Information (SII)

SII takes the concept of increased reporting one step further in that the reporting is completed in almost real-time. This is in comparison to either monthly or quarterly returns, which are the normal return periods.

On 1 July 2017, Spain introduced SII, which means that affected businesses are required to report all invoices – issued or received – to the Spanish tax authority within a four-day time limit via an electronic portal in a specified format.

Any business with an annual turnover of more than €6m in Spain, which belongs to a VAT group in Spain, or applies the “REDEME” scheme will fall under the SII regime (this applies equally to non-resident and non-established companies).

Real-time reporting is not a new concept for tax; in Brazil, the SPED (Sistema Público de Escrituração Digital) system was introduced for certain taxes and businesses in 2008 and has since been expanded with continuing success for the tax authorities in terms of tax revenue and compliance.

Comunicazione IVA trimestrale

Italy introduced a new reporting obligation in May 2017 that requires businesses to electronically communicate their VAT transactions every quarter. This includes every invoice that has been issued or received as well as the VAT data from each periodic payment period. The failure to present the data may result in a penalty of up to €25,000.

This replaces a system in which the tax authority previously only required an annual VAT return to be filed, alongside monthly or quarterly payments being made. As a result, the tax authorities now see data on a much more regular basis and hence can take steps to rectify what they see as errors in a more prompt manner.

How are the tax authorities working together?

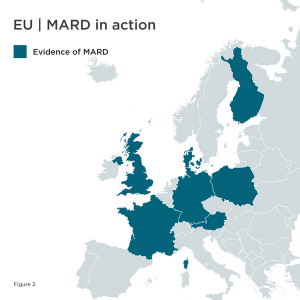

Not only are EU Member States introducing new reporting requirements that allow them to keep a closer eye on a taxpayer’s obligation to register for and declare the right amount of VAT within their own country, they are also now working together to help each other collect these debts. The Mutual Assistance for the Recovery of Debt (MARD) Directive was effected on 1 January 2012 and is a legislative tool used to recover debts in other Member States.

There has been an increasing number of examples where businesses are being sent letters from tax authorities across the EU that believe, from information they have obtained from each other and from third parties, that the company should be registered for VAT in their country. How tax authorities reach this decision and the information they use to justify it differs from country to country.

Listed below are some examples seen across Europe.

France

France has been known to collect post office data so that it can monitor the number of parcels being sent by traders. When it believes that a trader might have breached their distance selling threshold it can check to see if the trader meets its obligations. If they don’t, it will go after the trader utilising the MARD mechanism.

Germany

Germany has been taking a tough stance towards businesses that it believes should be registered, and is making it clear in communications that it is working with the UK tax authorities:

“If we do not receive the money you owe within 2 weeks after you received this letter, we will be forced to request the appropriate authorities in Great Britain to collect the amount overdue compulsorily. Furthermore outstanding debts of you clients will be impounded and your German VAT identification number will be deleted.”

Finland

In a recent case, an accountant’s client had received a letter from the Finnish tax authorities.

In this particular case, the tax authorities had set out that they had reason to believe that the company had more than likely breached the Distance Selling threshold in Finland. This position had been reached following the review of information obtained from “credit card and payment transfer companies”. The letter set out that the tax authority was planning to register the company on their behalf and had even estimated the VAT that it believed to be due.

Austria

The Austrian tax authority has recently been cracking down on distance sellers with retrospective issues by actively seeking out companies that it suspects may have breached the distance selling threshold since it was lowered in 2011. Companies have reported receiving letters from the tax authority prior to registering requesting information on their sales data to prove if they have or have not breached the threshold.

The Austrian tax authority also regularly investigating any company that it suspects may have breached the threshold earlier than stated on their registration application. Should a company declare the wrong date of breach, the tax authority may apply sanctions and will request that the full VAT due is paid. It is therefore recommended that data be thoroughly reviewed to avoid any discrepancies and make sure that the correct amount of VAT is declared straight away.

How will Brexit affect MARD for the UK?

After Brexit, nobody can be sure as to what the relationship between the UK and the EU will be like. It could be that MARD remains in place, or that the UK leaves completely, or that a new arrangement is implemented.

However, whilst there is a still certainty on the use of MARD, EU tax authorities are looking to collect money from UK businesses through the scheme ahead of the possibility of the ties being severed.

Businesses that communicate openly and honestly with the tax authorities, even when they are in a retrospective position, are treated much more leniently than if the Member States have to chase for the money that is owed to them.

Businesses should regularly review their sales figures to ensure that they are in a position to register for VAT as soon as they are obliged to do so, especially as the methods used by the tax authorities to track businesses they suspect should be paying local VAT are increasing and becoming more accurate.

Nicholas Hallam is CEO at Accordance.